If you’ve spent any time on a factory floor in Stuttgart or a hospital research wing in Amsterdam lately, you’ve probably noticed something: nobody’s impressed by a VR headset anymore. It’s not a novelty act wheeled out for a trade show demo. It’s just… a tool. Someone’s wearing it to check a wiring schematic on a half-built engine, or walking a trainee through a procedure they’ll perform on a real patient next week. That shift, from “look what we can do” to “this is how we do it now”, is the real story behind Europe’s spatial computing market in 2026, and it’s a story that hasn’t been told nearly as often as the consumer headset headlines.

So let’s actually dig into it: what’s happening, who’s leading, why Germany keeps showing up at the top of every report, and what it means if you’re trying to understand where this market goes next.

What “Spatial Computing” Actually Means in a European Context

Before going further, it’s worth being precise about the term, because “spatial computing” gets used as a catch-all for augmented reality (AR), virtual reality (VR), mixed reality (MR), and increasingly, the AI layer sitting on top of all three. In practice, when European market analysts talk about spatial computing, they mean the full stack: the headsets and smart glasses, the software platforms running on them, and the services layer- consulting, integration, training content- that turns hardware into something a business can actually deploy at scale.

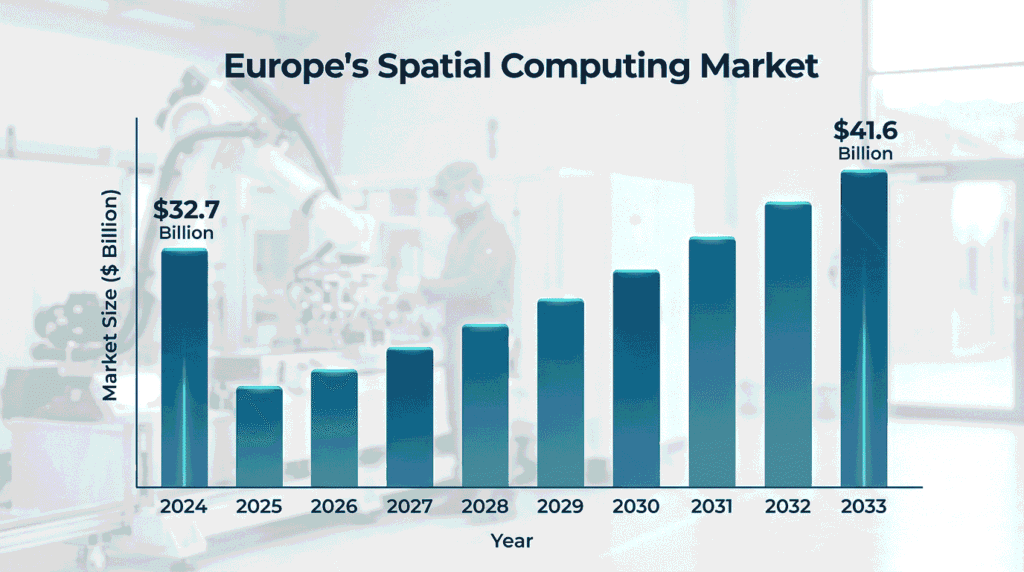

That distinction matters because Europe’s growth story isn’t primarily a hardware story. According to market research firm MarketDataForecast, the European spatial computing market was valued at roughly $32.8 billion in 2024 and is projected to climb to around $41.6 billion by 2033, growing at a compound annual rate just under 20%, and a large share of that growth is coming from the services and software layers wrapped around enterprise deployments, not from consumer headset sales (MarketDataForecast, 2025). Put plainly: Europe isn’t trying to out-ship Meta’s Quest line. It’s trying to out-deploy everyone else in manufacturing, healthcare, and industrial training.

Why Germany Keeps Topping Every Report

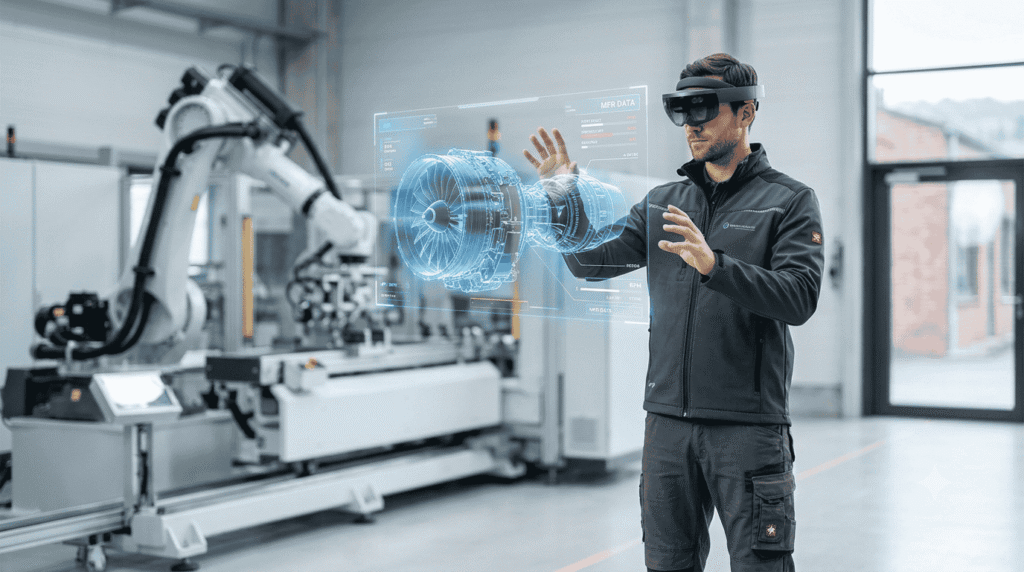

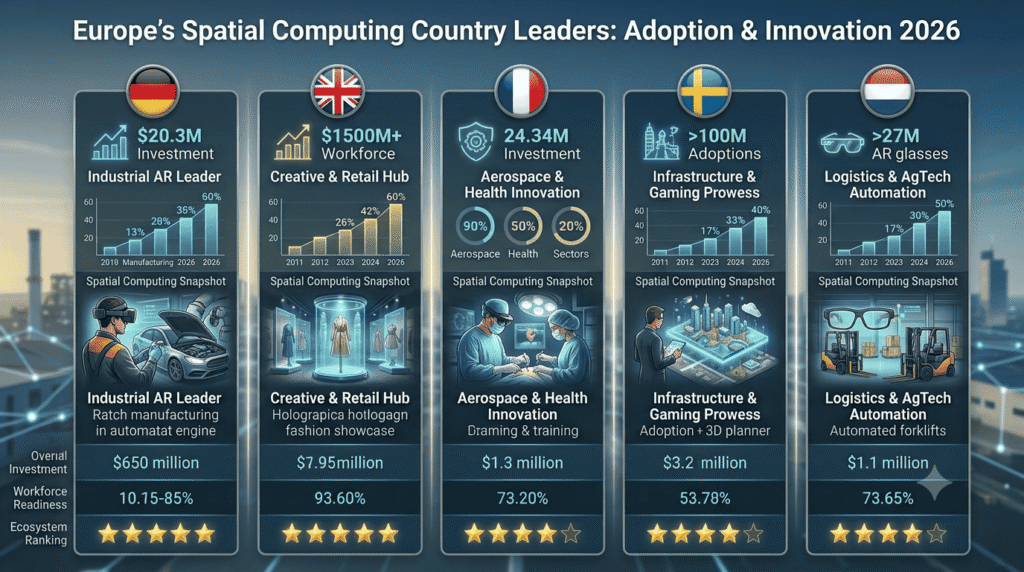

If you read enough of these market reports, and we read a lot of them while researching this piece, one country shows up first almost every time: Germany. That’s not a coincidence, and it’s not just about GDP size. Germany has spent the better part of a decade building “Industry 4.0,” its national push toward smart, connected, sensor-rich manufacturing, and spatial computing slots into that strategy almost perfectly. Assembly-line workers use mixed reality headsets for hands-free maintenance guidance. Engineers walk through digital twins of machinery before a single physical part is built. Training programs that used to take a new hire two weeks to absorb on a real production line can now happen in a simulated environment first, with mistakes that cost nothing instead of mistakes that cost a halted line.

The UK is close behind, but for a slightly different reason: it has both a strong enterprise AR/VR ecosystem and a genuinely deep technology investment base concentrated around London. Fortune Business Insights and other forecasters expect the UK’s extended reality market to reach close to $15.8 billion by 2026 on its own, driven heavily by enterprise software and a regulatory environment that, post-Brexit, has moved relatively quickly on digital transformation policy compared to some EU member states (Fortune Business Insights, 2025).

France tells yet another story, one driven less by manufacturing scale and more by deliberate government policy. French government-backed digital innovation programs have specifically targeted immersive technology as a strategic sector, and the country’s strong design and creative-industries culture gives spatial computing applications in architecture, fashion, and product design a natural home. It’s also worth flagging Dassault Systèmes here, the French software giant whose 3D design and simulation platforms have become genuinely foundational to how European industrial firms approach digital twins- not flashy, but enormously influential.

Sweden and the Netherlands round out the leading group, both growing quickly thanks to strong research ecosystems, dense startup networks, and, particularly in the Netherlands, heavy adoption in logistics and smart-warehouse applications, where AR-guided picking and inventory systems are quietly becoming standard rather than experimental.

The Healthcare and Manufacturing Engine

It’s tempting to assume that gaming and entertainment drive the AR/VR market, because that’s where consumer attention goes. In Europe specifically, that assumption is wrong. Healthcare and manufacturing are the two verticals doing the heavy lifting. The European Commission’s own 2024 Digital Industry Scoreboard documented growing deployment of mixed reality tools specifically in advanced manufacturing settings, things like remote-assisted maintenance, where a technician on the factory floor can see expert guidance overlaid directly on the machine in front of them, cutting both repair time and the need to fly in a specialist (European Commission Digital Industry Scoreboard, cited in MarketDataForecast, 2025).

On the healthcare side, surgical planning and medical training applications are where most of the serious investment is going. Surgeons are increasingly using AR-assisted visualization to overlay CT or MRI imagery directly onto a patient before or during a procedure, something that sounds futuristic until you realize it’s already standard practice in a growing number of European teaching hospitals. We cover this in more depth in our piece on virtual reality in healthcare, which is worth reading alongside this one if hospital-specific applications are what brought you here.

The Friction Points Nobody Talks About

No honest market overview skips the hard parts, so here they are. The single biggest structural challenge in Europe’s spatial computing market isn’t demand, it’s standardization. Because so many devices, platforms, and software ecosystems have developed independently, interoperability is genuinely difficult. An AR maintenance application built for one headset manufacturer’s platform frequently won’t run cleanly on another’s, which means European enterprises evaluating a spatial computing rollout often have to commit to a single vendor’s ecosystem earlier and more fully than they’d like.

Cost is the second friction point, and it disproportionately affects education. The European Commission’s Digital Education Action Plan has actually proposed a dedicated spatial computing access fund for vocational schools, explicitly because hardware costs currently keep meaningful classroom deployment confined to elite institutions and large corporations rather than the broader school system. As of early 2026, implementation of that fund remains pending, which tells you something honest about the gap between strategy documents and budget reality in EU digital policy.

And then there’s the regulatory layer, which in Europe is both a friction point and, longer-term, probably a competitive advantage. The EU’s broader approach to data protection and AI governance means spatial computing companies operating here have to think hard about biometric data, eye-tracking data, and spatial mapping data from day one, rather than retrofitting privacy compliance later. It slows initial rollout. It also means European enterprise buyers are, on average, more confident in the compliance posture of the tools they’re adopting than buyers in markets with looser rules.

How This Compares Globally

It’s worth a quick zoom-out, because numbers in isolation don’t mean much. The global spatial computing market overall is forecast at somewhere between $202 billion and $221 billion in 2026, depending on which research firm’s methodology you trust, with most projections pointing toward the market crossing the $1 trillion mark sometime between 2034 and 2035 at a compound annual growth rate north of 20% (Precedence Research, 2025). North America currently holds the largest single regional share, somewhere around 32% to 46% depending on the source, largely because that’s where Meta, Apple, Microsoft, and Google are headquartered and where the bulk of consumer hardware revenue lands. Asia-Pacific is the fastest-growing region in percentage terms. Europe sits in a strong but distinctly different lane: smaller in raw consumer hardware revenue, but disproportionately strong in enterprise deployment depth, which is arguably the more durable kind of market position to hold as the initial hardware hype cycle settles.

If you want the Asia-Pacific side of this comparison in detail, India’s training boom, Japan’s robotics crossover, Singapore’s smart-nation programs, we’ve broken that down separately in Spatial Computing Market in Asia-Pacific 2026. And if Gulf markets are on your radar instead, our piece on Spatial Computing in the Gulf: Why Dubai and the UAE Are Moving Faster covers a region that’s taking a very different, government-led approach to the same underlying technology.

What to Watch Through the Rest of 2026?

A few specific things are worth tracking if you’re following this space closely rather than just reading one report and moving on. First, watch whether the EU’s proposed vocational-school spatial computing fund actually gets implemented, because it’s a genuine bellwether for whether policy ambition in this space translates into real classroom hardware, something that’s been a recurring gap in European digital education initiatives generally. Second, keep an eye on interoperability standards efforts; if a credible cross-platform standard emerges in 2026, it could meaningfully accelerate enterprise adoption by removing the single-vendor lock-in problem described above. Third, manufacturing-sector digital twin adoption in Germany and the broader Industry 4.0 corridor (Germany, Austria, northern Italy) is likely to keep setting the pace for what “mature” enterprise spatial computing deployment looks like across the rest of the continent.

Key Takeaways

Europe’s spatial computing market is growing at nearly 20% a year, but the engine behind that growth is enterprise deployment, manufacturing, healthcare, and industrial training, not consumer headset sales. Germany leads on the strength of its Industry 4.0 manufacturing base, the UK is close behind on enterprise software and investment depth, and France is carving out a distinct lane through government-backed digital innovation programs and its design-industry strengths. The real obstacles aren’t demand-side; they’re standardization, hardware cost (especially in education), and the genuine, if double-edged, complexity of building within the EU’s stricter data and AI governance framework. None of that changes the trajectory. It just means Europe’s version of this market will keep looking less like a gaming trend and more like infrastructure.

Frequently Asked Questions

What is the size of the European spatial computing market in 2026?

Europe’s spatial computing market was valued at roughly $32.8 billion in 2024 and is projected to reach approximately $41.6 billion by 2033, growing at a compound annual rate of nearly 20%.

Which European country leads in spatial computing adoption?

Germany leads, driven by its Industry 4.0 manufacturing strategy and heavy enterprise investment in mixed reality for training, maintenance, and digital twins. The UK and France follow closely, each via a different path: enterprise software investment in the UK’s case, government-backed innovation programs and design-industry adoption in France’s.

What industries drive spatial computing demand in Europe?

Manufacturing and healthcare are the two largest drivers, followed by automotive, education, and logistics, not gaming and entertainment, which dominate consumer headlines but represent a smaller share of Europe’s actual market value.

References